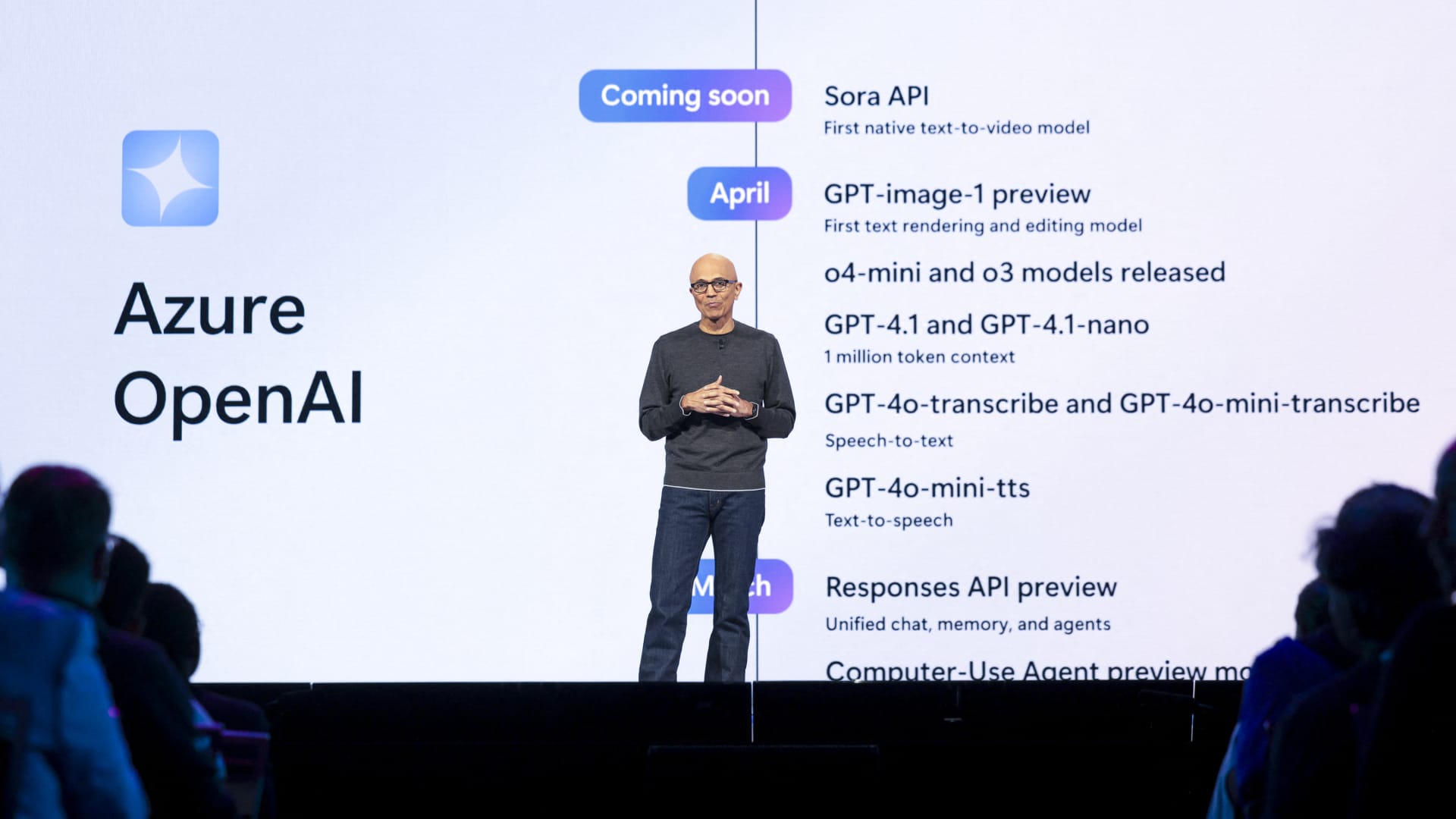

A strong start to the third-quarter earnings season has propelled the stock market back to record highs. Investors are hoping an even busier week of corporate reports — oh, and a Fed meeting — can keep the good times rolling. A wild card: President Donald Trump is in Asia for some high-stakes diplomacy. The S & P 500 ‘s record close Friday, its first since Oct. 8, came despite a lingering government shutdown that has created an economic data vacuum — Friday’s softer-than-expected inflation report notwithstanding — and rekindled trade tensions. While investors will keep an eye on shutdown negotiations in the week ahead, the deluge of earnings will dominate the conversation on Wall Street. Nearly a third of the Club’s portfolio will be among those reporting, so we’ll have our hands full. Another tall task will be monitoring the headlines out of Trump’s trip to Asia, where he’s expected to hold a face-to-face meeting with Chinese President Xi Jinping. 1. Earnings: Here’s what we’re expecting from the 10 Club holdings reporting this week. All estimates for revenue and earnings per share are as of Friday and sourced from financial data provider LSEG. Corning: The maker of fiber optic cables and iPhone screen glass kicks off the jam-packed week of earnings Tuesday morning. When we started the position in Corning last week, we intentionally kept it on the small side ahead of the quarter — even though we do expect to see a strong set of results. The crux of our thesis is that Corning’s optical communication enterprise business is a big winner in the AI data center buildout, so that’s an important box to check this quarter. We’ll also pay close attention to the results of and commentary around its specialty materials segment, home to its iPhone business, as a potential read-through to iPhone 17 demand. Analysts are looking for earnings of 66 cents per share on revenue of $4.23 billion. Boeing : When the aircraft maker reports Wednesday morning, delivery rates will be a key watch item, particularly for the 787 wide-body model and the narrow-body 737 Max, the latter of which the Federal Aviation Administration recently allowed Boeing to increase production to 42 per month. A ramp in cash flow in the coming years is the real question for investors, but delivery rates will influence the timing of that ramp. On the other hand, we are anticipating a multibillion-dollar charge for its 777x program. However, the Street is aware of this and, as a result, it should be baked into the estimates. For example, analysts at JPMorgan are estimating that the charge will be about $4 billion. Accordingly, the consensus is for a loss of $5.15 per share on revenue of $21.97 billion. On free cash flow, a highly influential metric for Boeing, analysts are expecting a negative $626 million. Starbucks : The coffee chain is still very much a turnaround story. The results were mixed last quarter, but as we noted in late July, we saw signs of stabilization and were encouraged that seven of its top 10 markets outside the U.S. were able to deliver positive same-store sales growth. We are looking for a slightly cleaner quarter this time around, though we understand comebacks like this can be messy. CEO Brian Niccol has said the second quarter was largely about figuring out what steps needed to be taken to get the company back on track for long-term success. As a result, we’re interested to see what has been implemented since then. Also of interest will be commentary regarding how Starbucks can innovate and bring newness to its menu that draws in new customers. For example, we want to hear the initial response to Starbucks’ recently launched protein initiative . Analysts are expecting Starbucks to report earnings of 57 cents per share on sales of $9.36 billion. Meta Platforms : While most are expecting strong topline results and solid user engagement, it’s the cost side of the equation — both capital expenditures and operating expenses — that will garner investor focus and drive the stock reaction on Wednesday night. Up to this point, investors have largely been accepting of Meta ‘s immense AI spending, and CEO Mark Zuckerberg is clearly going to spend big on what he (and we) believe is possibly the most consequential technology of our lifetime. However, the return on all this spending is still something investors are on edge about. As a result, any discussion of increased spending — as the commentary on its Q2 call indicates we’ll see next year — should be accompanied by a commentary on demand signals or efficiency gains the company is seeing that justify further investment. Lastly, though Meta wearables are too small to move the needle at the moment, we want to hear commentary on adoption trends because it may turn into a serious revenue generator over time, especially if Meta’s more affordable Ray-Ban collaboration helps build brand loyalty among early adopters. The consensus is for earnings per share of $6.68 on revenue of $49.37 billion. Microsoft : As always, cloud unit Azure’s growth will be key to the stock reaction for Microsoft . That’s especially true given the amount of spending being done on AI infrastructure and clear signs that the spending doesn’t appear ready to let up anytime soon. Azure grew 39% last quarter, and the company’s guidance for the soon-to-be-reported quarter was 37% in constant currency. Regarding AI initiatives, we’re interested to hear any updates regarding the company’s relationship with OpenAI, following the memorandum of understanding signed by both companies in September. Don’t forget: The initial stock move on Microsoft’s release is always a knee-jerk reaction. The real move doesn’t come until about 30 minutes into the conference call, when CFO Amy Hood provides guidance for the current quarter. Wall Street expects the tech giant to report earnings of $3.67 per share on revenue of $75.33 billion. Eli Lilly : The uptake of Lilly’s blockbuster GLP-1s — Mounjaro for diabetes and Zepbound for obesity — will drive the share price reaction on Thursday morning. CVS’s decision to exclude Zepbound from insurance coverage took effect at the start of the quarter Eli Lilly is about to report. Analysts at Deutsche Bank say “the brunt of Zepbound’s exclusion from CVS’s template plans has largely played out,” but we’re interested in what management has to say about the overall competitive dynamics in GLP-1s. Additionally, analysts will likely pepper management with questions about oral GLP-1 orforglipron, a potential driver of growth next year and beyond. Lastly, any commentary regarding Washington’s efforts to cap the price of weight-loss drugs and lower the price of prescription drugs in general is welcome. The consensus is for earnings of $5.86 per share on revenue of $16.04 billion. Bristol Myers: Along with the headline results, we’re focused on sales trends for the schizophrenia drug Cobenfy. The drug’s upcoming late-stage trial readout on Alzheimer’s psychosis is arguably even more important for long-term investors. The data is due by year-end, and it is the biggest near-term catalyst for the stock. After Cobenfy suffered a setback in a separate trial earlier this year, a successful one here could help improve sentiment. Wall Street is projecting Bristol Myers to report earnings of $1.54 per share on revenue of $11.82 billion. Amazon: AWS results are key following last quarter’s results, when Amazon’s public cloud offering reported slower growth than its main competitors, Microsoft and Google. While AWS is the biggest cloud by revenue, investors hoped to see more following the performance of rivals. Wall Street expects AWS growth of 18.1% in the third quarter, versus 17.5% in the June-ended period, according to FactSet. Are the workloads of AI startup Anthropic, whose largest backer is Amazon, helping stoke AWS growth? Investors are also now speculating that Anthropic is the fourth big customer working with Broadcom on custom chips. Anthropic’s cloud deal with Google also figures to be a topic of conversation on the call. On the retail side, in addition to any commentary the company can provide on the consumer, we’re interested to learn more about how management is implementing the use of robotics. The New York Times reported on this last week, and analysts at Morgan Stanley estimate Amazon’s embrace of robotics could result in savings of $2 to $4 billion by 2027, with potentially much greater efficiency gains beyond that timeframe. Recall, CEO Andy Jassy did previously highlight the potential savings and workplace transformation resulting from the implementation of AI and robotics. The third leg of the Amazon growth stool right now is advertising, and the consensus is for 21% growth in the third quarter. On a companywide basis, the Street is expecting Amazon to deliver earnings of $1.58 per share on revenue of $177.72 billion. Apple: Demand for iPhone 17 is top of investors’ minds, even if the reported quarter includes only about a week of sales. Expectations are not priced into the stock, which is still underperforming the broader S & P 500. Services revenue growth is also a key watch item because its high-margin profile has an outsized impact on overall earnings results. Lastly, any timeline for Apple’s AI initiative is crucial to the longer-term story. Apple is expected to report earnings of $1.77 per share on revenue of $102.12 billion. Linde: Linde is one of those companies that doesn’t get much news coverage, and it’s way too high up in the supply chain to be exciting. But its standing as a leading supplier of industrial gases provides management with a 30,000-foot view of demand dynamics in various end markets across the globe. That includes more resilient consumer-oriented end markets, such as health care, food and beverage, and electronics, as well as more cyclical industrial end markets, such as manufacturing, chemicals and energy, and metals and mining. With its fingerprints all over the economy, we covet what Linde executives have to say about both the company’s operations and the other industries in which we’re invested. That’s especially true against the backdrop of a government shutdown that starved the market of a host of economic data. Within the financials, we’ll be looking for cash flow to rebound. We’ll also be keeping an eye on the backlog as it provides insight into future growth. Lastly, while China isn’t expected to show much improvement, we’re curious if the team is seeing any rebound coming in 2026. The consensus is for earnings of $4.18 per share on revenue of $8.61 billion. 2. Federal Reserve: At its penultimate meeting of the year, the Fed on Wednesday afternoon is widely expected to deliver another quarter-point rate cut, which would bring its overnight lending rate down to the range of 3.75% to 4%. The market is also pricing in a near-certain cut at its December meeting, according to the CME Group’s FedWatch tool . Friday’s cooler-than-expected consumer inflation report didn’t materially change the odds for this week’s meeting, but for December, they went to 96% from 91%. While the stock market certainly will appreciate the Fed’s cut, investors need to remember that the bond market has a mind of its own — it will not always move in lockstep with the central bank. We saw that in September, when the Fed began its cutting cycle and the yield on the 10-year Treasury moved higher, just as it did a year ago. The good news this time around is that the 10-year Treasury yield has come back down to below 4%, south of where it was when the Fed cut last month. Additionally, given the lack of official government data during the shutdown, Fed Chair Jerome Powell’s usual post-meeting conference call will take on another level of intrigue as the market looks for insights into where the central bank believes the economy has trended in the past few weeks. 3. Trade : Trump arrived in Malaysia over the weekend to kick off the longest overseas trip thus far in his second presidency. He’s also scheduled to travel to Japan and South Korea, where he’s expected to meet with China’s Xi to talk trade on Thursday. With the recent pickup in U.S.-China tensions, the market will hope for a Trump-Xi meeting that puts the world’s two largest economies back on better footing. Top of mind for investors: Will there be any updates on the flow out rare earth minerals out of China and the flow of American-designed semiconductors into China?”I think we have a really good chance of making a very comprehensive deal,” Trump told reporters traveling with him on Air Force One, according to The Associated Press . “I want our farmers to be taken care of. And [Xi] wants things also.” Week ahead Monday, October 27 Dallas Fed Index at 10:30 a.m. ET Before the bell: Keurig Dr Pepper (KDP), Bank of Marin Bancorp (BMRC), Carter’s, Inc. (CRI) After the bell: Nucor Corp. (NUE), Rambus, Inc. (RMBS), Avis Budget Group, Inc. (CAR), WM (WM), Amkor Technology, Inc. (AMKR), NXP Semiconductors N.V. (NXPI), Whirlpool Corp. (WHR), Alexandria Real Estate Equities, Inc. (ARE), Cadence Design Systems, Inc. (CDNS), Crane Co. (CR), Bed Bath & Beyond, Inc. (BBBY), Brown & Brown Inc. (BRO), Welltower Inc. (WELL), Ameris Bancorp (ABCB), Arch Capital Group Ltd. (ACGL) Tuesday, October 28 S & P Cotality Case-Shiller Home Price Indices at 9 a.m. ET Richmond Fed Index at 10 a.m. ET The Conference Board’s Consumer Confidence Survey at 10 a.m. ET Before the bell: Corning (GLW), Sherwin Williams (SHW), UnitedHealth Group, Inc. (UNH), SoFi (SOFI), PayPal (PYPL), United Parcel Service, Inc. (UPS), Celestica, Inc. (CLS), Carrier (CARR), D.R. Horton, Inc. (DHI), HSBC Holdings plc (HSBC), Royal Caribbean Cruises Ltd. (RCL), JetBlue Airways Corporation (JBLU), VF Corp. (VFC), Applied Industrial Technologies (AIT), Ares Capital Corp (ARCC), NextEra Energy Inc (NEE), Wayfair Inc. (W) After the bell: Enphase Energy Inc (ENPH), ONEOK Inc. (OKE), Bloom Energy Corporation (BE), Booking Holdings Inc. (BKNG), Seagate Technology plc (STX), Visa Inc (V), Electronic Arts Inc (EA), Meritage Homes Corporation (MTH), Cheesecake Factory (CAKE), Community Healthcare Trust Incorporated (CHCT), Caesars Entertainment, Inc. (CZR), Edison International, Inc. (EIX), Mondelez International Inc. (MDLZ) Wednesday, October 29 The Federal Reserve’s interest rate decision at 2 p.m. ET Fed Chair Jerome Powell’s post-meeting press conference at 2:30 p.m. ET Before the bell: Boeing Co. (BA), Otis (OTIS), Verizon Communications (VZ), GE Healthcare (GEHC), CVS Health (CVS), Fiserv, Inc. (FI), Centene Corporation (CNC), Caterpillar, Inc. (CAT), Etsy, Inc. (ETSY), Automatic Data Processing, Inc. (ADP), American Electric Power (AEP), Phillips 66 (PSX), Amarin Corporation plc (AMRN), Criteo S.A. (CRTO), Cognizant Technology Solutions Corp. (CTSH), Brinker International, Inc. (EAT), Garmin Ltd. (GRMN), GlaxoSmithKline plc (GSK), Chart Industries Inc. (GTLS), Kraft Heinz Company (KHC) After the bell: Starbucks Corp. (SBUX), Meta Platforms, Inc. (META), Microsoft Corp. (MSFT), Alphabet Inc. (GOOGL), Chipotle Mexican Grill Inc (CMG), Google (GOOG), Carvana Co. (CVNA), ServiceNow, Inc. (NOW), MercadoLibre Inc (MELI), Sprouts Farmers Market, Inc. (SFM), Agnico-Eagle Mines, Ltd (AEM), Green Brick Partners Inc. (GRBK), Coeur D’Alene Mines Corp. (CDE), Stem, Inc. (STEM), Align Technology, Inc. (ALGN), eBay, Inc. (EBAY) Thursday, October 30 Before the bell: Bristol Myers (BMY), Eli Lilly & Co. (LLY) , Mastercard (MA), Merck & Co., Inc. (MRK), Insmed, Inc. (INSM), Comcast Corp. (CMCSA), CommScope Holding Company, Inc. (COMM), Enterprise Products Partners L.P. (EPD), Blue Owl Capital Inc. (OWL), Roblox Corporation (RBLX), Advance Auto Parts Inc. (AAP), Baxter International, Inc. (BAX), Shake Shack Inc. (SHAK), Southern Company (SO) After the bell: Amazon.com, Inc. (AMZN), Apple, Inc. (AAPL), Coinbase Global, Inc. (COIN), Reddit, Inc. (RDDT), Western Digital Corp. (WDC), MicroStrategy, Inc. (MSTR), Rocket Companies, Inc. (RKT), Riot Platforms, Inc. (RIOT), Cloudflare, Inc. (NET), Roku Inc (ROKU), First Solar Inc (FSLR), Atlassian Corporation Plc (TEAM), Twilio, Inc. (TWLO), Gilead Sciences, Inc. (GILD) Friday, October 31 Chicago PMI at 9:45 a.m. ET Before the bell: Linde (LIN ), Exxon Mobil Corp. (XOM), Chevron Corporation (CVX), AbbVie Inc. (ABBV), Canadian National Railway Company (CNI), Charter Communications Inc. (CHTR), LyondellBasell Industries (LYB), AON Plc (AON), Cboe Global Markets, Inc. (CBOE), Church & Dwight Co., Inc. (CHD), Dominion Energy, Inc. (D) (See here for a full list of the stocks in Jim Cramer’s Charitable Trust.) As a subscriber to the CNBC Investing Club with Jim Cramer, you will receive a trade alert before Jim makes a trade. Jim waits 45 minutes after sending a trade alert before buying or selling a stock in his charitable trust’s portfolio. If Jim has talked about a stock on CNBC TV, he waits 72 hours after issuing the trade alert before executing the trade. THE ABOVE INVESTING CLUB INFORMATION IS SUBJECT TO OUR TERMS AND CONDITIONS AND PRIVACY POLICY , TOGETHER WITH OUR DISCLAIMER . NO FIDUCIARY OBLIGATION OR DUTY EXISTS, OR IS CREATED, BY VIRTUE OF YOUR RECEIPT OF ANY INFORMATION PROVIDED IN CONNECTION WITH THE INVESTING CLUB. NO SPECIFIC OUTCOME OR PROFIT IS GUARANTEED.