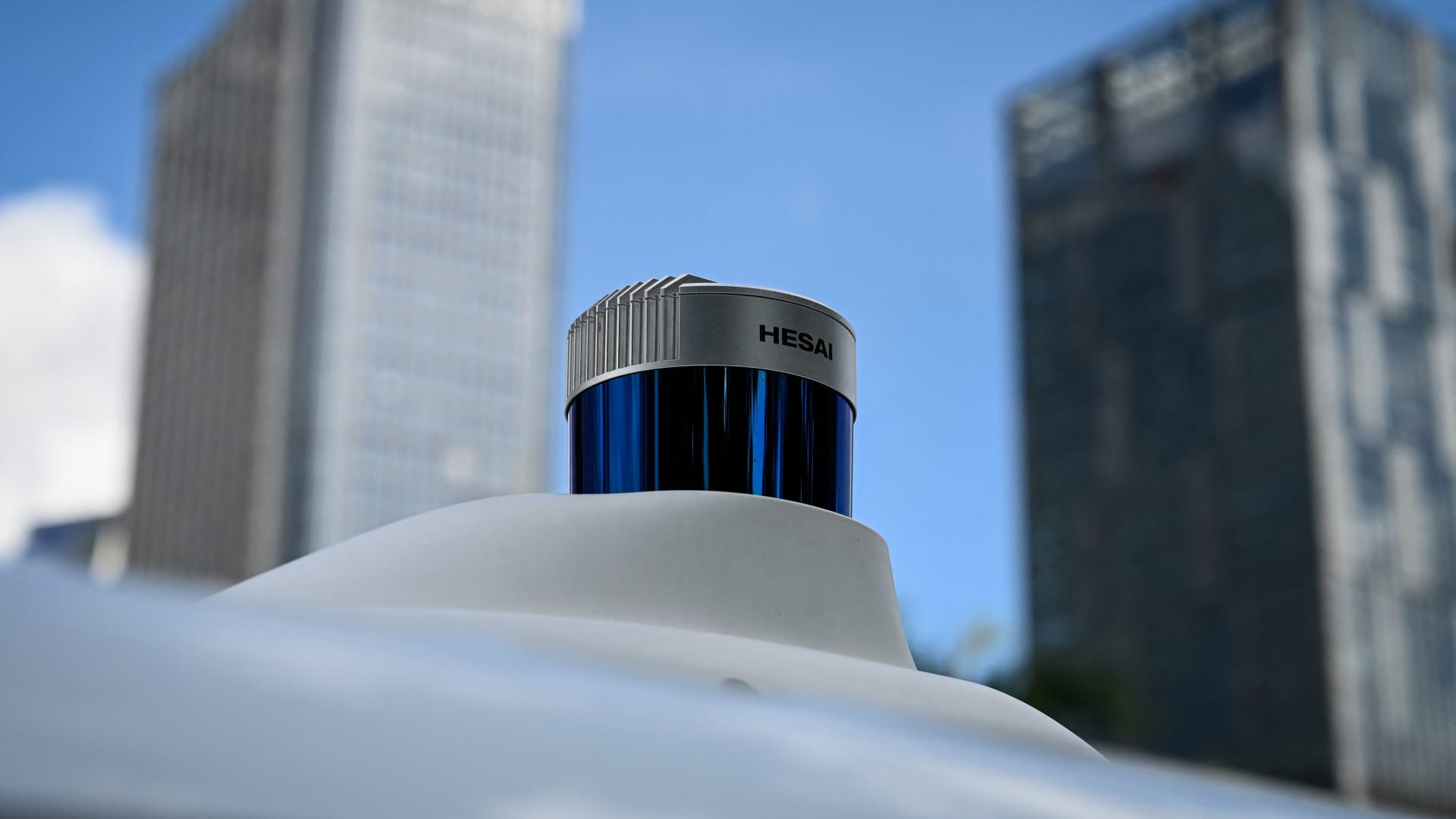

Goldman Sachs likes Chinese automaker supplier Hesai for the long run as the company grows its global footprint and enters a new product cycle. Analyst Tina Hou upgraded Hesai to buy from neutral. She also hiked her price target on U.S.-listed shares to $18.40 from $5.50. The new forecast suggests roughly 34.9% upside from Monday’s close. Hesai is a provider of high-performance lidar technology that makes products for advanced driver assistance systems, autonomous technology and industrial robots. The company had 37% revenue market share in the global lidar industry in 2023, per Goldman. Lidar is a technology employs laser pulses to measure the distance to a target, and it is used to create three-dimensional models and elevation maps of the real world. “We believe Hesai is well-positioned to benefit from China NEV market’s NOA (navigation on autopilot) adoption acceleration starting from 2025E, together with the launch of lower-cost products, to drive LiDAR usage by mass-market vehicle models,” Hou said. “We believe the market hasn’t factored in the operating leverage from new product cycle,” Hou said, adding that the stock’s valuation is “attractive” at current trading levels. The analyst noted the stock trades at 20 times 2026 earnings, below the global smart EV supplier average of 30 times. The upgrade follows Hesai’s roughly 10% fall during Monday’s trading session, after Morgan Stanley downgraded the stock and said its upside appears limited even though the company has a robust project pipeline ahead of itself. Looking ahead, Goldman remains confident in Hesai’s growth in NOA adoption, which the firm predicts will have 67% year-over-year growth in terms of vehicle equipment as ADAS enters into a “take-off” phase from 2025 to 2030. The company is also entering the “harvesting stage” of its new three-year product cycle for its next-generation platform lidar product called ATX, Hou pointed out as another catalyst for shares. Shares popped more than 6% in the premarket following the upgrade. Overall analyst sentiment is mixed on the stock. LSEG data shows that nine of 10 who cover it rate it a buy or strong buy. However, the average analyst price target signals 31% downside. Hesai is coming off a strong year, rising 55% in 2024.